As recently highlighted in our report in collaboration with AWS, embedded finance is the next battleground in the experience economy - enabling any brand, business, or merchant to integrate innovative financial services into its propositions and customer experiences. It is predicted to become a $7.2 trillion opportunity in the next 10 years, twice the combined value of the world's top 30 banks today.

Technology has fuelled growth of “on-demand” services and “super apps” in recent years, offering customers access to a range of products/services such as food, transport, groceries and e-commerce, instantly at their fingertips and all in one place. With the on-demand economy expected to reach $335 billion by 2025, the likes of Uber, Deliveroo, Gojek and Grab have woven themselves into consumers’ daily lives across multiple geographies and reached multi-billion dollar valuations.

With the exponential growth of the on-demand economy and a largely untapped embedded finance opportunity, how can on-demand businesses and aspiring super apps get a piece of the ~$7 trillion pie? Here is a three-step approach to help kickstart and shape this journey.

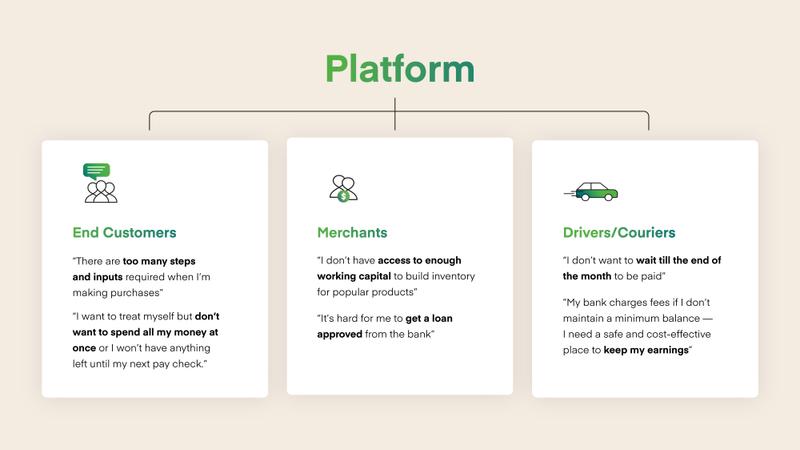

1. Define core stakeholder groups and their challenges/needs

It all starts with the customer problem or need to be addressed. On-demand platforms typically serve three core stakeholder groups (and hence three distinct sets of “customers”):

- End customers: end users who are consuming products and services offered on the platform (e.g., booking rides, ordering food and products)

- Merchants: businesses who offer products or services to end customers via the platform (e.g., restaurants, grocery stores)

- Drivers and couriers: delivery partners who link customers and merchants by offering pick up and delivery of products and services

Each of these groups will have specific challenges or needs to be addressed. Based on research conducted by Mambu’s Advisory team, examples of typical challenges faced by these groups across selected EMEA markets are highlighted in the infographic below.

2. Define objectives and principles for financial services opportunities

On-demand businesses are broadly optimising for three key outcomes – delivering a best-in-class customer experience, growing usage/adoption of the platform and creating “stickiness” to the platform and its services; thus acquiring new users, keeping existing users loyal and engaged and growing the strength of the ecosystem for all stakeholders. Any strategy for embedded financial services should look to complement this and follow a set of key principles:

- Drive synergies with core business: complementary offerings to align with business focus areas and drive positive spillover on the platform

- Enhance engagement intensity: ability to drive new and existing users to the platform by enhancing frequency and depth of user interaction

- Build once, deploy many: easily replicable propositions across geographies and markets with the ability to tweak for local nuances with minimal cost and effort (e.g., regulatory requirements)

While embedded finance can evolve into a core profit-generating avenue for on-demand businesses, the initial objectives and focus should be towards growing and strengthening the overall ecosystem while solving for immediate stakeholder needs.

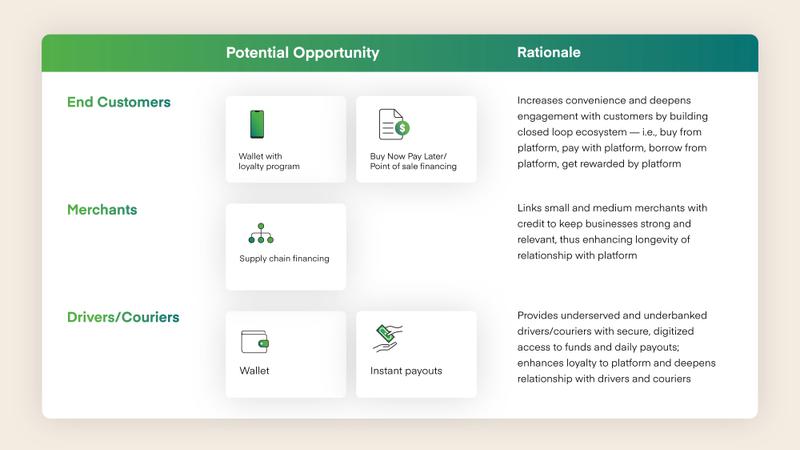

3. Shortlist and assess highest impact short-term opportunities

Based on the needs of the stakeholder groups and principles for embedded financial services, on-demand businesses can shortlist relevant use cases to roll out. Through our research and industry conversations, we have identified potential high impact opportunities to kick off the embedded finance journey (this could differ by market/region based on local nuances and user needs):

Loyalty-based digital wallets have grown exponentially during Covid with Worldpay projecting that this will account for >50% of consumer spending by 2024. Loyalty-based wallets are a proven starting point, with super apps such as Grab and Gojek demonstrating success with this in South East Asia. For example, the Grab Pay wallet was Grab’s first foray into financial services, enabling end customers to pay and get rewarded for consumption of various platform services - it has since evolved into a separate unit called Grab Financial Group and now offers a wide range of financial products for various stakeholders.

Point-of-sale financing is expected to reach $182 billion in value at an 18-20% annual growth rate by 2023, according to McKinsey estimates. Additionally, Buy Now Pay Later users are much more active and engaged compared to traditional card users when looking at metrics such as transaction volumes and length of relationship (2x and 1.5x higher respectively), which are in sync with core objectives of on-demand platforms.

From the merchants’ perspective, supply chain financing can unlock access to working capital to grow businesses, support timely payments towards outstanding invoices and enhance overall commercial viability of the business. The World Economic Forum projects a $2.5 trillion funding gap in trade finance by 2025 - on-demand platforms can help address this gap with their merchants by providing credit directly or facilitating access to financing for them via partners. For example, Amazon utilizes its own balance sheet and also partners with other banks to provide loans to small businesses selling on its platform.

For drivers and couriers, the introduction of instant payout capabilities has seen successful adoption. Most prominently, Uber launched Instant Pay to provide drivers with immediate payouts and real time access to funds through their existing bank account or dedicated Uber wallet, leading to $1.3 billion in cash outs within the first year of launch.

To kickstart the embedded finance journey and maximise chances of success, it is also important to:

- Build a business case to ensure benefits (e.g., customer engagement and retention, revenue per customer) outweigh or at least equal build and run costs

- Proceed with a focused, iterative rollout starting with 1-2 pilots with a single stakeholder group before rolling out at scale

- Test, gather feedback and refine offering(s) based on user feedback - more importantly, such customer input will also help define the longer term roadmap for financial services

- Identify necessary capabilities and requirements (e.g., technology, people, capital, licensing) and think through buy vs. build vs. partner considerations based on future aspirations

The race for financial services on demand has begun. Those that are prepared to lead from the front can win - and win big.

To find out more about embedded finance opportunities, read ‘Embedded Finance: Who will win the battle for the next digital revolution?’.