ARTICLE

Everything about SEPA payments schemes

This article was updated in April 2025

In this article, we examine SEPA payments from various angles. We begin by reviewing the four payment schemes and their common characteristics. We then explore SEPA payments in numbers, tracing their history and members across Europe, and finish by introducing the key stakeholders who keep it running.

The different SEPA payment schemes

The first SEPA payment scheme was introduced in 2008, called SEPA Credit Transfer. Since then, SEPA’s functionality has since expanded significantly.

Today, SEPA also offers instant transfers, direct debits for consumers and businesses, and the ability to request a transfer. In this section, we take a look at the SEPA payment schemes as they stand today, and how the SEPA payment schemes differ.

SEPA Credit Transfer

The first SEPA payment scheme, SEPA Credit Transfer (commonly shortened to SCT) simply enables a payment sent by the debtor (or payer) to the creditor (or payee).

It has a maximum execution time of one business day and a maximum credit time of two business days, from the moment it has been instructed by the debtor to its PSP. SEPA credit transfers are only processed during business days and business hours.

There is no minimum or maximum amount. No fees can be deducted from the payment, which means that the full amount is always credited on the creditor’s account.

A SEPA credit transfer can be recalled by the originator PSP within 10 business days for technical reasons, such as duplicate sending or technical problems, and within 13 months in case of fraud.

SEPA credit transfers are used for a variety of everyday use cases, including consumer-to-consumer bank transfers, regular salary payments, and insurance disbursement payouts.

SEPA Instant Credit Transfer

SEPA Instant Credit Transfer (shortened to SCT Inst) is the most recent SEPA payment scheme. It is a much faster version of a SEPA credit transfer, with a maximum time to credit of 10 seconds. SEPA instant credit transfers are processed entirely automatically, and around the clock.

The debtor’s bank is notified by the creditor’s bank that the payment has been credited on the creditor’s account, which enables the bank to notify its customer in return.

Unlike a SEPA credit transfer, a SEPA instant credit transfer cannot be repudiated. It cannot be cancelled and cannot be returned. It thus offers a much higher level of guarantee to the creditor.

SEPA instant credit transfers enable new use cases such as on-demand salary advances, real-time health insurance repayments, emergency payments, and secure online purchases. SCT Inst also enables companies to reduce working capital requirements and improve cash flow by collecting payments faster.

SEPA Direct Debit Core and Direct Debit B2B

Common characteristics of a SEPA payment

SEPA payments are highly standardised, with scheme rules set by the European Payments Council (EPC) and updates released every year. Though every SEPA scheme has unique characteristics, there are five characteristics common to every SEPA payment.

Euro as the sole currency

All SEPA payments are made in euros. The euro was introduced in 2002 as a single currency, and is currently the official currency of 20 out of the 27 EU member states and more than 350 million citizens. It is the second most used currency in the world, after the US dollar and before the Chinese yuan.

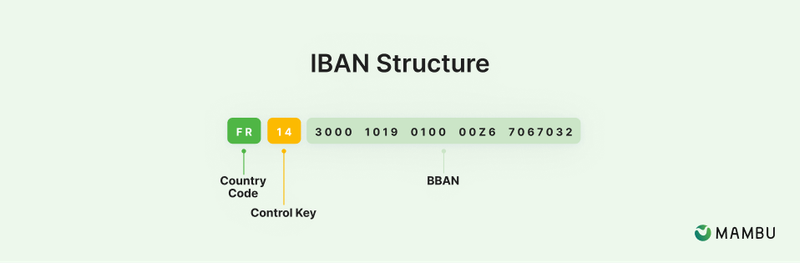

IBANs as account identifiers

IBANs (for international bank account numbers) are used to normalise account numbers across more than 80 countries, including the 36 countries that form the SEPA zone. However, several major countries including the US, Canada, Australia, China, and Japan are yet to adopt IBANs.

SEPA payments use IBANs as the sole way to identify debtor and creditor accounts. IBANs are meant to facilitate account identification, payments, and international trade by using a common syntax and format. The IBAN format is defined by the ISO 13616 standard. IBANs always start with a two-letter country code, followed by two check digits, and end with the BBAN (basic bank account number).

Both SEPA direct and indirect participants can issue their own IBANs and open and hold accounts in the name of their customers. PSPs often see issuing their own IBANs as a way to further strengthen their brand as well as customer relationship.

The length of an IBAN depends on the country. Some countries can be chatty (such as France, with 27 characters), while others can be more straight to the point (such as Belgium, with 16 characters). IBAN formats per country can be found in the appendixes of this guide.

Although the syntax of an IBAN can be verified using a basic algorithm, there is no built-in mechanism in SEPA to verify that the account exists and can be used for a given payment. A SEPA payment to a valid IBAN can therefore result in a rejection or return, for instance, if the account has been closed, does not exist, or is not compatible with the payment method used.

BICs as bank identifiers

Bank identifier codes (or BICs) are used to identify PSPs across the SEPA zone. BICs are registered and managed by SWIFT, a global financial messaging network.

The BIC code structure is specified by the ISO 9362 standard. BICs take the form of eight (also called BIC8) or eleven (also called BIC11) characters. A BIC8 identifies a PSP in a given country or city, while a BIC11 identifies a PSP’s exact branch. The BIC usually includes the PSP shortened name in the bank code.

SEPA payments by the numbers

Since the first SEPA payment method launched in 2008, the euro value of SEPA payments has grown rapidly and they dominate today the eurozone payment landscape by payment value.

In this section, we look at the state of the overall eurozone payment landscape. We also examine where, by volume and by value, SEPA payments fit in compared to other common payment methods in the eurozone, while looking at the progress made by the newer SEPA payment methods.

A note about SEPA statistics

Payment statistics in the SEPA are maintained by the ECB and published every year in July for the previous year. There are some limitations to this data when it comes to understanding payments executed throughout SEPA. There is no data available for SEPA direct debit B2B as well as SEPA instant credit transfer payments. Additionally, payment statistics for euro payments in non-euro countries and non-European Economic Area countries are not available.

2024 Payment Landscape

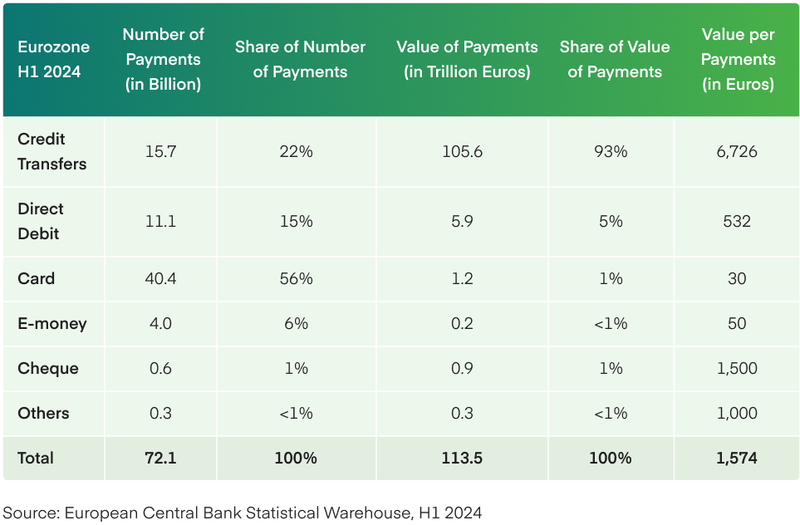

In the first half alone of 2024, the total number of non-cash payments in the eurozone, including all payment methods, increased to 72.1 billion, up 7.4% from the same period in 2023. The corresponding total value rose to €113.5 trillion, up 1.9% from H1 2023.

During H1 2024, the number of credit transfers within the euro area increased to 15.7 billion (up 6.5%) and their total value reached €105.6 trillion (up 2.0%). The number of direct debits increased to 11.1 billion (up 4.4%) with a total value of €5.9 trillion (up 2.6%).

Card payments accounted for 56% of the total number of payments, while credit transfers made up 22% and direct debits accounted for 15% of all transactions.

Credit transfers dominated in value, accounting for at €105.6 trillion in total value and 93% of total payment value. The next two largest methods by value were direct debits (5%) and card payments (1%).

These figures reflect the ongoing shift towards electronic payment methods in the euro area, with card payments leading in volume and credit transfers in value.

SEPA Payments

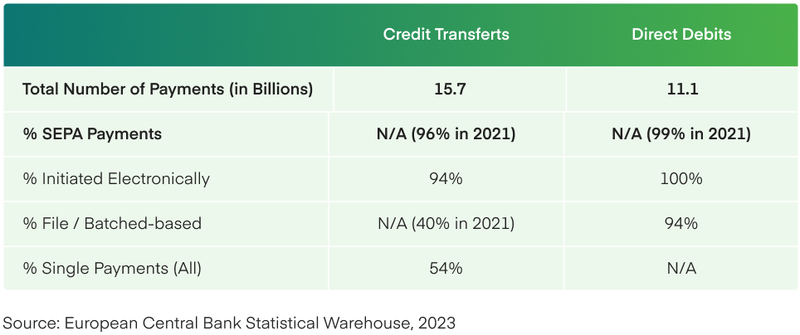

In 2023, SEPA credit transfers and SEPA direct debits core continued to account for the vast majority of transfers and debits sent in the eurozone in volume, having accounted for respectively 96% and 99% of all transfers and debits in 2021. The remaining payments are processed via other schemes. Credit transfers remain overwhelmingly electronic: only 6% were initiated via paper or in-person orders, a figure that has remained stable since 2021. Among SEPA credit transfers, approximately 54% were executed as single payment orders (including online and mobile banking) in 2021, while 94% of SEPA direct debit continued to be executed in a file and batch manner as of 2023.

SEPA, its history, and its members

SEPA was introduced for credit transfers in 2008, direct debits in 2009, and instant credit transfers in 2017. Credit transfers (regular and instant) are used to send a payment from account A to account B. Direct debit is used to debit money from a third-party account B and credit it to account A, based on the authorisation granted through a direct debit mandate signed between the debtor and the creditor.

The development of SEPA is part of the mandate of the Eurosystem, a group composed of the European Central Bank (ECB) and national central banks of other eurozone member states. National central banks make the necessary market infrastructure available to the banks in their respective countries.

The European Payment Council (EPC) specifies the payment schemes used by payment service providers (PSPs) and operated by clearing and settlement mechanisms (CSMs). The EPC is not a regulator and does not have a mandate from the EU or any other political, legislative, or regulatory institution, but rather represents and defends PSPs in front of European institutions, such as the ECB.

SEPA member states

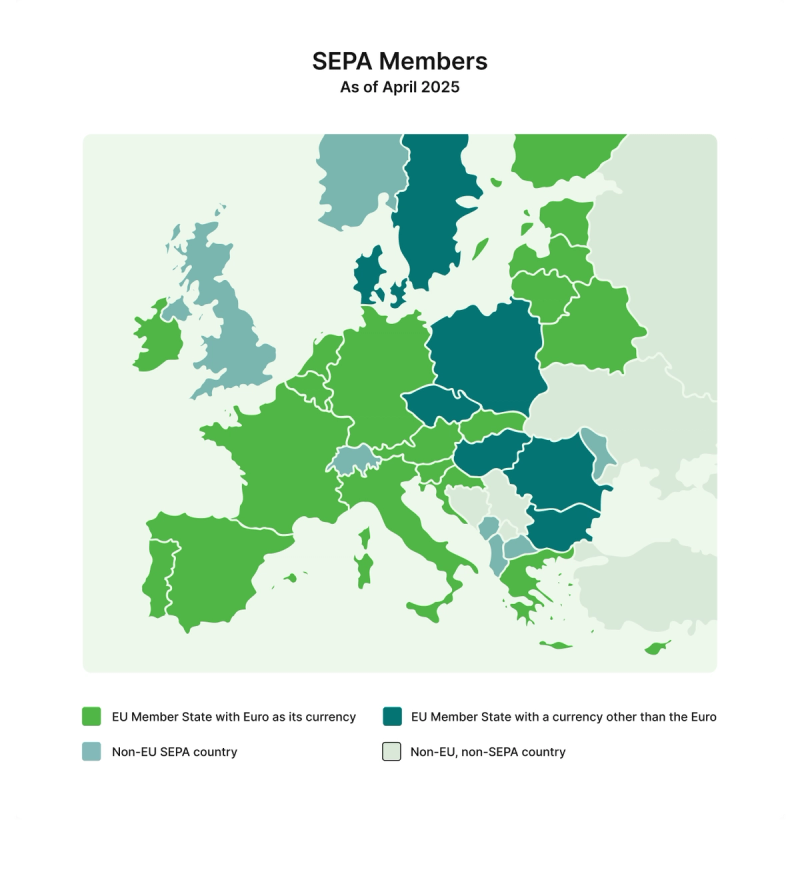

As of April 2025, the SEPA zone spans 40 European countries, including:

- 27 countries that are also members of the European Union (EU)

- 4 members of the European Free Trade Association (EFTA) —Liechtenstein, Norway, Iceland, and Switzerland

- 4 European microstates with special agreements with the EU — Andorra, Monaco, Vatican City, and San Marino

- The United Kingdom, which continues to participate in SEPA after it left the EU in 2020

- 4 countries in the process of EU accession that have joined SEPA – Albania, Montenegro, Moldova, and North Macedonia (effective as of October 2025)

Of these 40 countries in the SEPA zone, 13 do not use the euro as their official currency. Only payments sent and received in euros in these countries can be made as SEPA payments. Payments sent and received in local currencies to and from these countries use other local or international payment schemes and are not SEPA payments.

The different stakeholders involved in SEPA

Several organisations are involved in standardising and operating SEPA payments, but who are they and how exactly is each organisation involved in SEPA?

In this section, we outline the key organisations behind SEPA. We examine the role each organisation plays and look at how those actors involved in a SEPA payment fit together under SEPA’s four-corner model.

Regulatory bodies

The Single Euro Payments Area (SEPA) is governed by two supranational organisations - the European Commission, and the European Payments Council.

European Commission

The European Commission, with inputs from the ECB and the European Payments Council (EPC), is responsible for drafting the regulations and directives that form the legal and technical framework for SEPA.

European Payments Council

Founded in 2002 as a not-for-profit association and now counting 77 members, the EPC is responsible for harmonising payments across Europe. The EPC specifies the payment schemes used by payment service providers (PSPs) and operated by clearing and settlement mechanisms (CSMs). The EPC is not a regulator and does not have a mandate from the EU or any other political, legislative, or regulatory institution, but rather represents and defends PSPs in front of European institutions, such as the ECB.

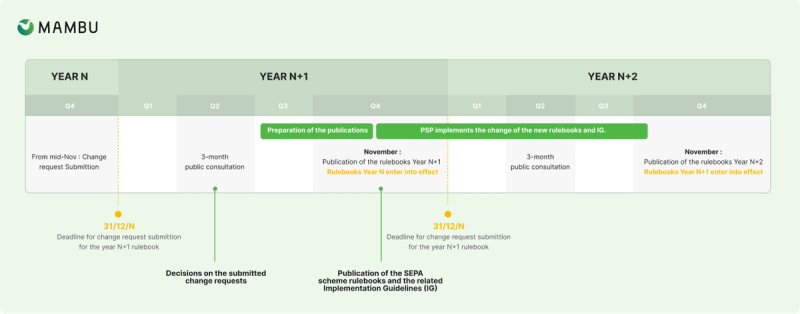

The role of the EPC is to provide the technical framework for each SEPA payment scheme. One of the key publications of the EPC is the SEPA rulebook. SEPA rulebooks define the business rules and technical standards which oversee each SEPA payment scheme.

New rulebooks are published every year in November and come into effect in November of the following year. When a new rulebook comes into effect, SEPA participants as well as CSMs are expected to update their systems and processes by implementing new validation rules and adjusting existing ones as well as supporting new SEPA message formats.

Actors involved in the execution of a SEPA payment

Every SEPA payment involves a number of actors: the originator and the beneficiary, the PSPs holding their accounts, and clearing companies. Software providers function to connect the different actors involved in a SEPA payment.

Four-corner model

© Mambu 2026