ARTICLE

The state of cash management APIs in Europe’s top banks in 2023

One of the major obstacles to SEPA instant payment adoption - which stands as of September 2022 at 13% of all credit transfers - has been the speed of transformation of the banking infrastructure.

Instant payments require application programming interfaces (or APIs) for end-to-end straight through processing. But implementing those APIs has proven to be a complex task for banks building on their legacy systems.

In this article sharing the learnings from a Numeral analysis of European banks APIs, we talk about the journey towards API for European banks and share an overview of the available cash management APIs and instant payment APIs currently offered as of November 2022 by banks. Discover the 21% of European banks with high API readiness, with which to build your next payment workflows.

How companies currently execute payments through their banks

The majority of B2B payments are still initiated today through payment files, pooling together hundreds of payments before sending the aggregated payment files to the bank. In the European Union, 40% of SEPA credit transfers and 94% of SEPA direct debits are initiated through payment files.

These files are generated by ERPs or in-house systems, approved and sent to the bank’s server through secure transmission protocols like EBICS or SFTP. Files are regularly recovered and processed by the bank which generates payment status reports to update its customers’ on the status of their payment orders. While very robust, the whole process involves many asynchronous steps, each adding delays to the payment processing.

To add more flexibility to payment operations teams, banks have started to build APIs for their cash management and this trend was accelerated by the introduction of the second Payment Service Directive (PSD2).

How PSD2 made bank APIs mandatory

PSD2 is a European legislation on consumer and business payments which was written into law for most European countries in January 2018.

At the same time, banks were mandated to create standard APIs for those emerging PSPs to access consumer information and initiate transactions with banks. From that intent, multiple API standards emerged for banks. The three most well known are the Berlin Group’s NextGenPSD2 (Germany and Austria), Open Banking (UK), and STET PSD2 (France). The fragmentation of API standards is seen today as one of the main challenges of EU open banking in its current form.

Independently of the implementation, PSD2 APIs enable three main use cases for PSPs:

- Account and transaction data: Access transaction and account data for an authenticated customer

- Payment initiation: Initiate a SEPA credit transfer from an authentified customer account. Customers authenticate in their banking environment to approve the payment

- Confirmation of funds: Confirm the ability of funds on a given customer account without initiating a payment

Certain use cases like e-commerce checkouts have hugely benefited from this new infrastructure, cheaper and with acceptable convenience when compared to cards. However when it comes to a company’s payment operations, those APIs have shown to be far from ideal for three reasons

- Limited scope: Only SEPA credit transfers are supported by most PSD2 APIs. And while this is clearly a topic for PSD3, payment methods like SEPA direct debits can’t be automated as of today.

- Strong authentication (SCA) requirement: With SCA requiring a manual approval per transaction or within a certain timeframe, true automation of payment flow is not an option for a business through PSD2 APIs.

- Reliability: For businesses processing thousands of payments per month, PSD2 APIs are not reliable enough and prone to break for large volumes of payments.

The current set of PSD2 APIs, while kicking off the march towards better connectivity, doesn’t come close to fulfilling the needs of treasury and payment operations teams. However, seeing APIs and connectivity as competitive differentiators, banks have started to build dedicated cash management APIs for their customers.

Banks are launching their cash management APIs

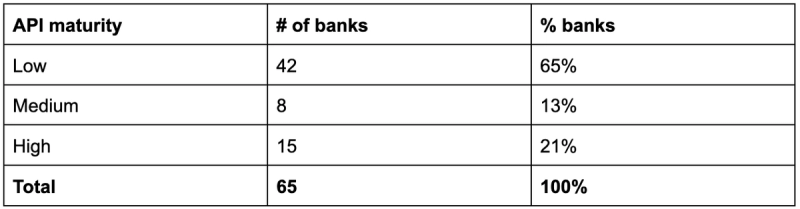

To better understand the current API landscape, we conducted in November 2022 a review of 65 major European banks (detailed methodology can be found at the bottom of this article).

We classified banks on three tiers depending on the maturity of their cash management APIs

- Low: The bank only has PSD2 APIs, but no dedicated cash management APIs for treasury and payment operations teams

- Medium: The bank has cash management APIs for certain use cases, but coverage is partial. For example, it could have for only one payment method or only be limited to querying account data

- High: The bank has a complete coverage of well documented cash management APIs

Over the 65 banks analysed throughout Europe, only 21% of banks had a high API readiness.

Meet the banks with instant payments APIs

SEPA instant credit transfer is the latest payment method introduced in the EU in 2018. However, while 71% of banks have adhered to the instant payment scheme and can at least receive instant payments, only a handful of banks allow for their customers to send instant payments through their cash management channels. And a fraction of them actually have straight through processing APIs to do so.

Our study shows that only 13 banks out of the 65 had publicly documented instant payment APIs. For certain banks, instant payment was actually the first API exposed by the bank and it still coexists with more traditional payment channels like SFTP and EBICS.If you are looking for a banking partner with an instant payment capability through API, here is the list of the banks offering it.

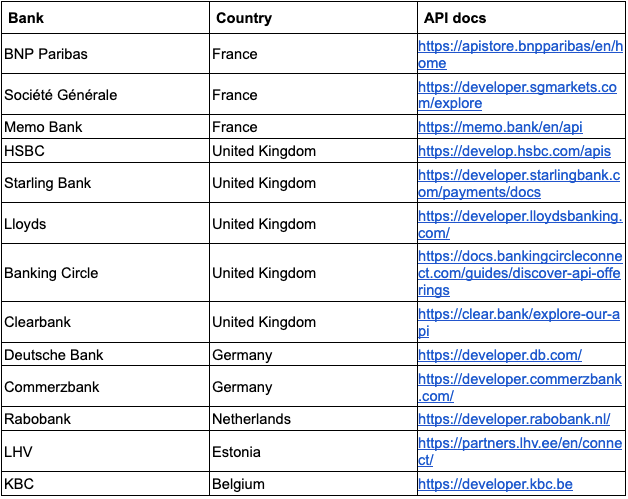

The banks with the highest API maturity are summarised in the following table.

How Mambu Payments accelerates the API-fication of banks

At the core of Mambu Payments are banks and real-time bank integrations. Mambu Payments securely connects to banks using direct connectivity channels (e.g. EBICS, SFTP, or messaging queues) and exchanges payment instructions, files and payment status reports, and account reports with the bank.

Mambu Payments then abstracts the diversity and complexity of bank protocols and file formats with a single API which is easy and quick to integrate and enables companies to build real-time, custom payment workflows.

Banks connected to the Mambu Payments platform are uniquely positioned to acquire and retain strategic customers and accelerate implementation projects through our API-first platform.

For payment operations teams, managing both instant payments as well as more traditional methods like credit transfers or direct debits requires the integration of multiple connectivity channels (API and SFTP). This extra development work creates friction to streamline operations and quickly adopt newer payment methods. Through Mambu Payments's single API, payment operations teams can reliably automate their payments with their banks.

Methodology

Mambu Payments researched the websites of the top 65 corporate banks in Europe and their publicly available API documentations. Research was conducted in November 2022. To get access to the full dataset, feel free to contact us.

© Mambu 2026