ARTICLE

The main differences between SEPA direct debit core and B2B

17 November 2022

SEPA Direct Debit Core (SDD Core) and SEPA Direct Debit B2B (SDD B2B) both enable regular payments for recurring obligations such as bills, rent, and subscriptions.

SDD Core is intended to enable all direct debit transactions, while SDD B2B is solely for recurring transactions between businesses or organisations. Functionally, both payment methods are similar but with key distinctions on the direct debit mandate management and refunds timelines.

In this article we outline how the SEPA direct debit payment schemes work, and how SDD B2B provides additional protections for businesses.

SEPA Direct Debit Core

A SEPA direct debit core (shortened to SDD core) is a payment pulled and debited from the debtor’s account and credited to the creditor’s account. SEPA direct debits are commonly used for recurring payments such as rent, utilities, software subscriptions, loan repayments, etc.

A SEPA direct debit core payment requires a mandate from the debtor to the creditor, which authorises the creditor to debit the debtor’s account under certain pre-agreed conditions. The mandate is identified by a unique mandate reference (or UMR). The creditor is identified by a creditor identifier, which is usually assigned by the national bank of the country of the creditor.

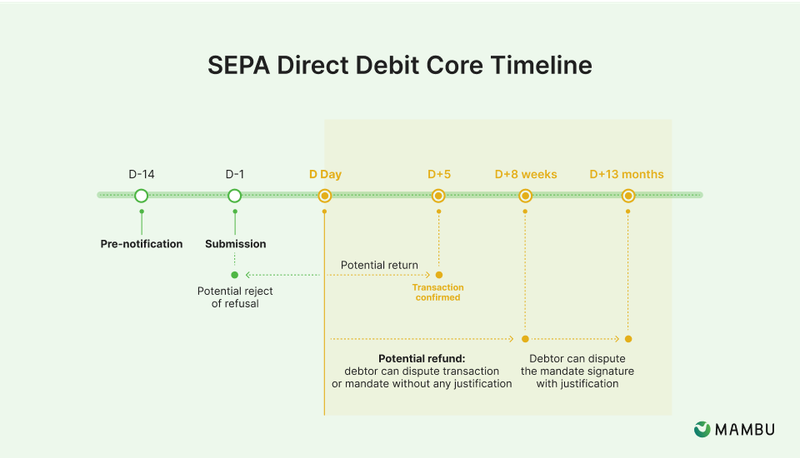

The payment must be initiated between two weeks and two business days before its due date. It can be rejected by the debtor’s bank until five days after its due date, for instance if the account has been closed. The debtor needs to be notified two weeks in advance of the settlement date unless the debtor explicitly waives the notification.

A SEPA direct debit can be refunded up to eight weeks after execution. In that period, a refund can be requested even if there was a valid mandate and even if the payment had been authorised. A refund can be then requested for up to 13 months after execution if there was no valid mandate, or if the payment was not authorised.

SEPA Direct Debit B2B

SEPA direct debit B2B payments are used between companies and with tax authorities. Common use cases include repaying loans, paying taxes, or paying for large purchases.

A SEPA direct debit business-to-business payment (called SEPA Direct Debit B2B, shortened to SDD B2B) is similar to a SEPA Direct Debit Core (SDD), with two major differences relevant for businesses: mandate verification and refund period.

Before a SDD B2B payment can be processed the mandate agreed between the parties must be sent to and registered by the debtor’s PSP. The requirement to register a mandate with the PSP does not apply to SDD Core payments, which makes SDD B2B payments unique in this respect. Furthermore, the debtor’s PSP is responsible for verifying that a SEPA direct debit B2B corresponds to a valid mandate before executing the payment and debiting the debtor’s account.

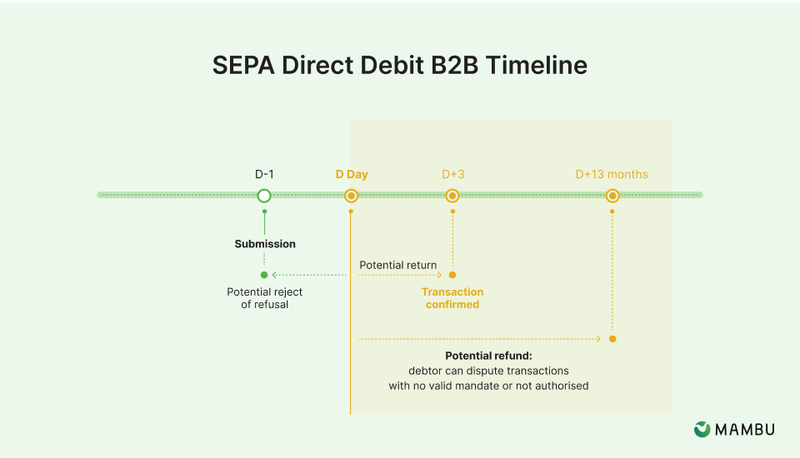

As a result of this extra step and the security implied for the debtor, a SEPA direct debit B2B payment cannot be refunded by the payer if there was a valid mandate and if the mandate had been authorised, unlike a SEPA direct debit core payment. A SDD B2B payment can still be refunded up to 13 months after execution if there was no valid mandate or if it was not authorised. The debtor’s PSP may still return the payment up to three days after the execution for technical reasons or because the debtor PSP is unable to accept the collection for other reasons, such as the account being closed, the customer being deceased, the account not accepting direct debit, or the debtor refusing the debit.

A SEPA direct debit B2B payment must also be initiated between two weeks and one business day before its due date. But unlike with a SEPA direct debit core payment, a pre-notification of the debtor is not required.

© Mambu 2026